Serving on the board of a nonprofit organization can be a labor of love. Whether you’re the President or Treasurer, you’re driven by a mission to make a meaningful impact.

However, as they say, “with great purpose comes great responsibility.” This is especially true when it comes to managing and protecting your nonprofit’s finances. A nonprofit financial risk assessment is a good way to safeguard against fraud, mismanagement and inefficiency—ensuring that every dollar contributes to your mission.

Proactively Addressing Financial Risk

Remedying the effects of fraud and mismanagement of funds can be cumbersome to say the least. Not to mention the damage to your reputation. By being proactive and mitigating risks, nonprofit leaders can ensure the protection of resources, build trust, and enhance efficiency and comply with regulations.

The key areas that you will want to focus on when it comes to assessing your current financial risk include:

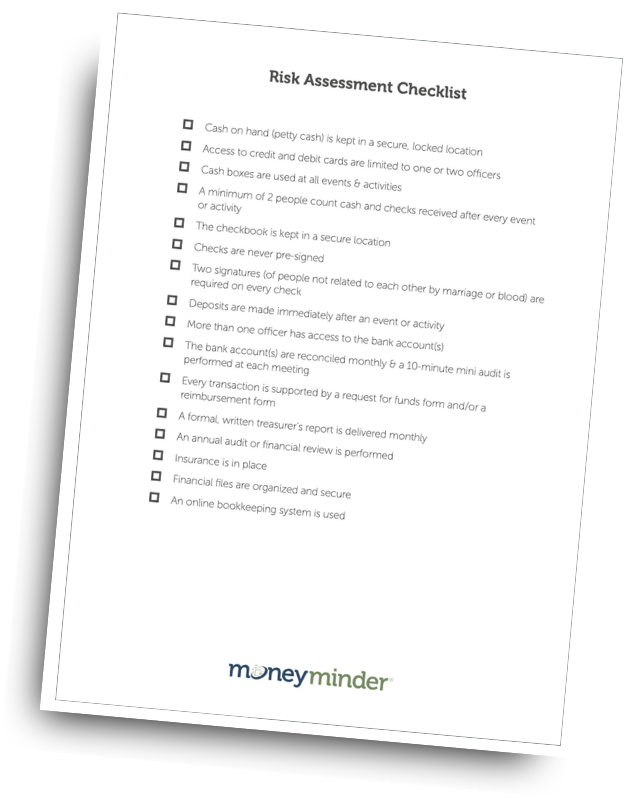

1. Handling Cash, Checks & Payments

Managing incoming and outgoing payments is a common source of financial risk for nonprofits. Implement clear procedures for cash handling, check issuance and electronic payments to minimize errors and opportunities for someone to “take a little off the top.”

2. Banking & Deposits

Certain protocols regarding check handling and bank deposits can go a long way in protecting you from risk. Make deposits immediately after an event, and always ensure more than one board member has access to the bank account(s). Regular reconciliation can help surface any inconsistencies before they get too out of hand.

3. Proper Bookkeeping

Ask any successful nonprofit and you’ll hear that accurate and up-to-date bookkeeping is the backbone of a financially sound organization. Implement a nonprofit accounting software such as MoneyMinder to ensure transactions are properly recorded, enabling you to track expenses and income effectively.

Start a free 30-day trial of MoneyMinder today.

4. Reporting & Audits

Regular financial reporting and audits are vital for transparency and accountability. They can help identify discrepancies and ensure everyone involved with the finances is on the same page. Some organizations require an annual audit.

5. Insurance

MoneyMinder does not sell or profit off of your group getting insurance. But we absolutely insist that your organization have adequate insurance coverage to protect against theft, fraud or lawsuits. This is a big one. We have quite a few articles and videos that talk about nonprofit insurance coverage, including this one from Cyndi’s Strong Treasurers, Strong Communities series.

Take Action: Get the Free Checklist

Risk prevention starts with awareness and preparation. Use this free, fillable nonprofit risk assessment checklist to help further create a culture of accountability and transparency in your organization. Your mission deserves nothing less than the highest standards of financial integrity.

Looking for more nonprofit resources? Head over to our Treasurer Resources shop for fillable forms, guides and docs to make your life easier.

Connect your Venmo account to MoneyMinder PRO to directly download transactions, saving you time and effort. You just review the transactions to ensure they are properly categorized and fill out any required fields.

Connect your Venmo account to MoneyMinder PRO to directly download transactions, saving you time and effort. You just review the transactions to ensure they are properly categorized and fill out any required fields. Connect your Bank, Paypal and Square accounts to MoneyMinder PRO to directly download transactions, saving you time and effort. You just review the transactions to ensure they are properly categorized and fill out any required fields.

Connect your Bank, Paypal and Square accounts to MoneyMinder PRO to directly download transactions, saving you time and effort. You just review the transactions to ensure they are properly categorized and fill out any required fields. Connect your Bank, Paypal and Square accounts to MoneyMinder PRO to directly download transactions, saving you time and effort. You just review the transactions to ensure they are properly categorized and fill out any required fields.

Connect your Bank, Paypal and Square accounts to MoneyMinder PRO to directly download transactions, saving you time and effort. You just review the transactions to ensure they are properly categorized and fill out any required fields. Join It is a membership management service that helps businesses and nonprofits effectively sell, track, and grow their membership.

Join It is a membership management service that helps businesses and nonprofits effectively sell, track, and grow their membership. Connect your Bank, Square and PayPal accounts to MoneyMinder PRO to directly download transactions, saving you time and effort. You just review the transactions to ensure they are properly categorized and fill out any required fields.

Connect your Bank, Square and PayPal accounts to MoneyMinder PRO to directly download transactions, saving you time and effort. You just review the transactions to ensure they are properly categorized and fill out any required fields.